Outline:

If you have been keeping up with thecollectibles newsat all, you know that 2025 was one of the best years ever, if not the bestcards, sneakers, comics, and other items of interest. The past few months have been particularly intense; companies that evaluate cards, specifically Collectors (the parent company of PSA, SGC, and now Beckett), have been evaluating cards at an extremely fast pace because of a significant rise in interest.

RELATED: 2025 Hobby Recap: Discounts, Controversies, and High-Value Card Sales

As per data from GemRate, the total volume of card grading increased by 32% compared to the previous year, highlighting how deeply embedded grading is in the hobby. In just December, approximately 2.43 million cards were graded by the five largest grading companies (PSA, CGC, Beckett, SGC, and TAG).

In 2025, a total of 26.8 million cards were evaluated by leading grading services, representing a 32% increase compared to 2024, which had 20 million cards. The largest portion, 71.8% (19.26 million), was graded by PSA, while CGC came in second with 18.4% (4.92 million).

PSA Domination

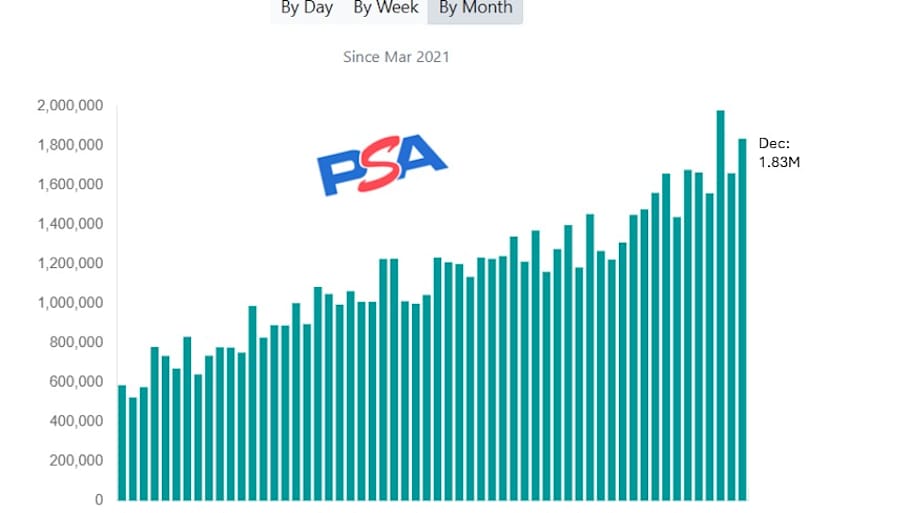

It’s no surprise that PSA maintained its dominance in the market, representing the majority of all graded cards. The brand continues to be the go-to option for many collectors, particularly in the sports category, and this position remains strong. Last January was PSA’s slowest month in 2025, with approximately 1.3 million cards graded, whereas October saw a peak just below 2.0 million. This pattern shows that demand increased as the year progressed, a trend observed across all grading companies.

PSA wasn’t only the leader in card volume in 2025. Along with experiencing its most successful year ever in terms of volume, they also won the title of Grading Company of the Year atMantel’s inaugural Hobby AwardsCompetition was intense, featuring CGC, C3 grading, SGC, and TAG, but PSA ultimately received the award.

Although PSA remained the leading entity in terms of volume, the significant percentage growth in 2025 was driven by other entities. Both CGC and TAG experienced remarkable year-over-year increases. CGC recorded an impressive 121% rise, while TAG achieved a solid 83% increase. These figures may indicate that collectors are becoming more open to distributing their submissions outside of PSA, possibly because of factors such as processing times, pricing models, cross-market opportunities, or trust in alternative grading options.

Introducing another element of mystery to the hobby is the consolidation narrative within the grading sector. Collectors, the parent company of PSA, recently acquired Beckett. Having Beckett under the Collectors’ ownership may alter competitive relationships in the future and has raised concerns among some collectors (and a congressman) regarding potential monopolistic practices.